After the start of Russia's ‘Special Military Operation’, sanctions on the Russian Federation from Western governments increased greatly. The sanctions also affected imports and raw materials, including important resources for the Russian capital and the world market, such as natural gas.

In June 2022, the chemical company, Linde, announced its withdrawal from a joint project with Gazprom to build an LNG terminal, and in September the Nord Stream 2 gas pipeline was blown up, which disrupted the pumping of gas from the Russian Federation to Europe. The Russian capital was almost completely squeezed out of the European energy market. It is not difficult to assume that Western raw materials corporations received the main benefit of this.

No matter what Western politicians say about their positioning in the Ukrainian events, Western capital took advantage of Russia’s ‘Special Military Operation’ and the “cancellation” of the Russian Federation to throw Gazprom out of Europe. They made huge profits from the struggle. Once again the Marxist law of imperialism was confirmed.

I. State of the market after sanctions

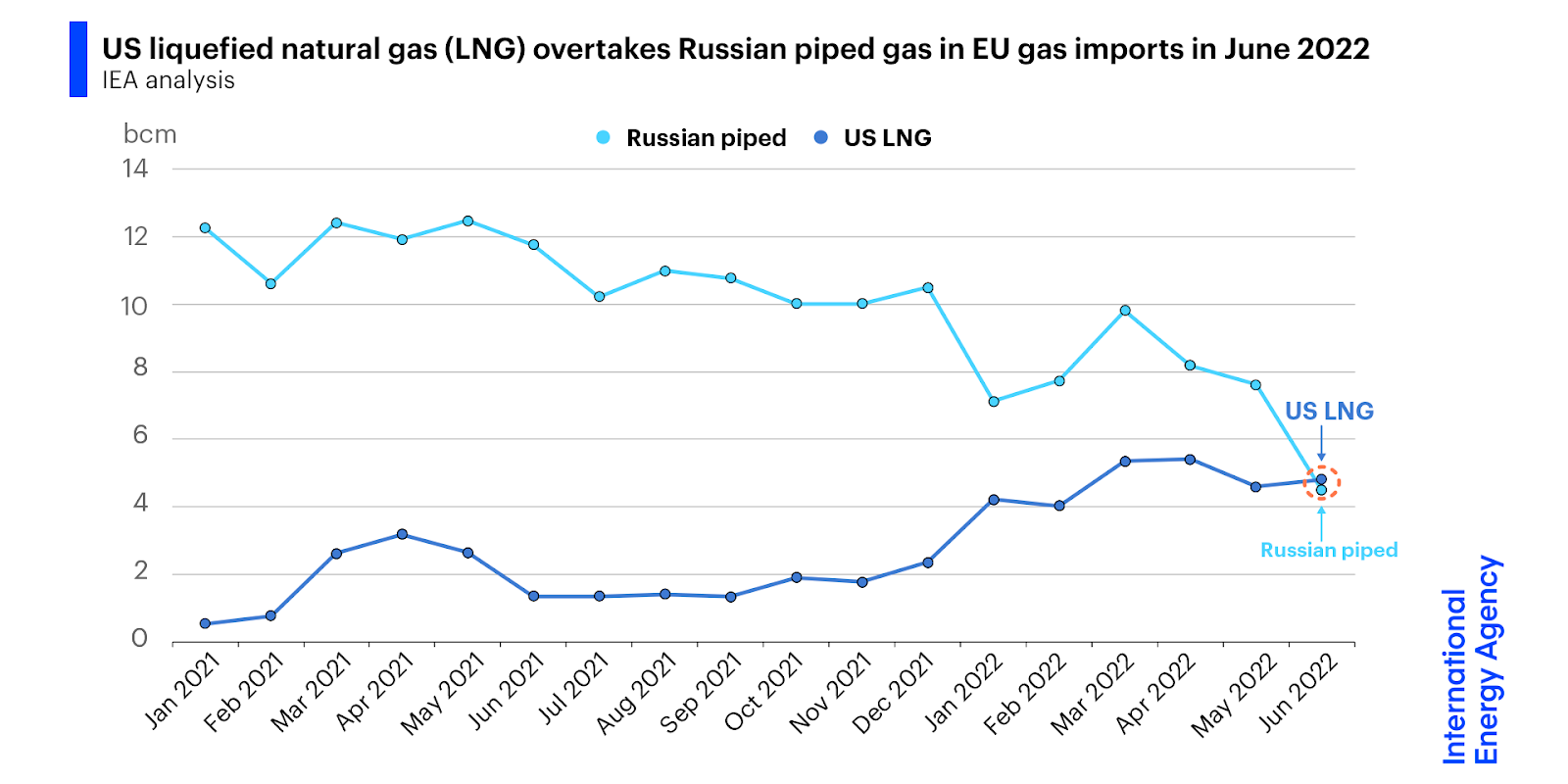

As Russian gas imports decreased, the volume of gas imports from Western countries, or from those countries that the so-called “collective West” considers its satellites, gradually increased. This gas is mainly of American and Norwegian origin.

For quite a long time, the resource policy of EU countries, including Germany, was focused on Russian gas. That, in turn, was supplied mainly by pipelines.

The radical ideas immediately put forward by the European Commission at the end of February - beginning of March 2022 to switch to the import of American liquefied gas were not only distinguished by the high cost of its use. These ideas were also fraught with difficulties in exploiting liquefied natural gas as an energy resource: the leadership of the Federal Republic of Germany was faced with the task of building LNG terminals and filling existing underground gas storage facilities with gas.

It is worth noting separately that this nuance, associated with the technical difficulties of switching from Russian to American gas, quite clearly revealed the difference in the positions of the ‘patriots’ and consistent communists on this issue.

The former, for almost a whole year, through the mouths of pro-government “military correspondents” and other “experts and analysts,” fed a large audience with mischief in the spirit of “Europe will definitely freeze.” The latter understood perfectly well that for 300% of the profit the capitalists were ready to put a noose around their neck. Even for this, they first have to build a terminal for receiving LNG.

Subsequent events showed the correctness of this second case: for the sake of wild profits, the Western capital built not one, but three floating LNG terminals. So, at the end of 2022 - beginning of 2023. LNG terminals in Wilhelmshaven and Lubmin were included in the connector. Further, on January 22, 2023, a terminal was built in the city of Brunsbüttel near Hamburg. What is most characteristic is that the last of the three LNG terminals that opened is completely private, a period in the mutual ownership of the French TotalEnergies and the German Deutsche ReGas.

Already at the beginning of January 2023, the first batch of American LNG in the amount of 170 thousand m³ arrived in Germany at one of the three terminals managed by the German state-owned company Uniper in Wilhelmshaven. This event became a key stage in the implementation of the plans of American raw materials corporations to redistribute and monopolize the European gas market. A ship called Maria Energy was loaded with LNG a month earlier in the United States, and the above volume of gas was enough to supply 50 thousand households.

However, the total capacity of all three terminals in the amount of 17 billion m³ per year or 47 million m³ per month is almost three times less than the former capabilities of Gazprom, and therefore it would be extremely naive to believe that this is the end of the ambitions of the new raw material hegemons of Europe. It is not without reason that at the end of March 2023 it became known that new exploration work was being carried out for the construction of new LNG terminals in the area of the German Baltic coast in the vicinity of the island of Rügen.

All the indignation of environmentalists and all kinds of European “greens” regarding the construction of terminals turned out to be in vain, and the entire “green agenda” of the European Union turned out to be hypocritical. Such large-scale work in the heart of the EU could not be carried out without the knowledge of the European Commission. This once again only confirms that under the conditions of the dominant capitalist system, what is “acceptable” from an environmental point of view and what is not is decided solely by the prospect of obtaining super-profits.

And these super-profits turned out to be possible with soaring gas prices already in the first months after the start of Russia's ‘Special Military Operation’. As a result of “unscrewing the valve,” the United States already in the first (!) half of 2022 took the place of the world’s largest exporter of LNG. As of mid-November 2022, according to the US Department of Energy, US LNG exports over 9 months exceeded 82 billion m³, of which 68% of supplies went to European countries.

The first record US LNG export was achieved at the end of the same month, reaching 362 million m³ per day, 11% higher than in 2021.

Measuring LNG volumes by tonnage, US LNG exports totaled 81.2 million tons during 2022, matching Qatar. Moreover, as in the case of Germany, at the end of January 2023, it became known about the construction of 5 more LNG terminals, in addition to the 11 that were already under construction. In total, during 2022, LNG supplies from the United States to Europe increased by 2.4 times compared to 2021. Thus, the United States occupied 40% of the European market at the beginning of February 2023.

The increase in LNG supplies from the United States was not at all prevented by the accident at the “blue fuel” processing plant in Texas, and the fabulous profits were not prevented by the indignation of even prominent European officials in Brussels. The latter circumstance was also explained by climatic reasons or, to put it figuratively, winter was upon us. However, in this case, the famous mantra of bourgeois mainstream economics is appropriately applicable: “Demand creates supply.” Indeed, the invisible hand of the market clearly pointed its finger at the new exporters of the “blue flower”.

However, unlike the fictional world in which bourgeois economists live, in the real world the price of a product, due to “market equilibrium,” does not necessarily imply a compromise between buyer and trader. Of course, supporters of all sorts of bourgeois economic theories may think otherwise, but the ordinary population of the EU, whose costs for paying electricity bills have increased noticeably, is unlikely to agree with them.

According to news from the Bloomberg news agency on December 18, 2022, Europe's losses due to the refusal of Russian gas reached $1 trillion.

According to available statistics, in Germany, at the same time, the share of Russian gas decreased to 20% per year, and gas consumption from Russia to 35%.

As you can see, the notorious “complete refusal” of Russian gas did not happen, but even these indicators turned out to be quite enough to fill the gap in raw materials. In this case, is it worth talking about the Czech Republic, in which by February 2023 the share of Russian gas had completely decreased from 97% to 4% in just a year?

In the second case, the gas is of Norwegian origin. Norway, along with the United States and Qatar, also joined the list of new exporting countries in 2022, skillfully taking advantage of “market conditions”.

When talking about Norway separately, we should especially note its colossal role in replacing Russian gas and oil. In addition, a purely technical point is particularly noteworthy: Norwegian gas is delivered by pipeline.

For example, on October 27, 2022, Poland joined the list of importers of Norwegian pipeline gas. It was on that day that the Baltic Pipe was put into operation. This gas pipeline has been under construction since 2001 and, having acquired particular relevance in light of the events of 2022, eventually ended up being laid through Denmark and the Baltic Sea. Operating at 30–38% of its capacity, the gas pipeline has an annual throughput capacity of 10 billion m³.

In this regard, it would be useful to recall the fact that pipeline gas supplies to Poland were stopped from the Russian side in response to the refusal to pay in rubles (or rather, to open a correspondent ruble account with Gazprombank) in July 2022. Thus, it was the Russian oligarchs who, with their own hands, pushed the “brother Slavs” into the arms of “spiritless Western neo-colonialists.”

Speaking about Germany as a measure of export opportunities, supplies of Norwegian gas there have increased by 11% compared to 2021. However, as pointed out by DW, Norway had to reduce supplies to the UK to achieve this.

If until August 2022 in the energy sector of Germany, the proportion of Russian gas to Norwegian gas was 55% to 35%, then Norway has now become the main supplier of gas to Germany. It was only at the beginning of April 2023 that it became known that Norway was not considering the construction of new gas pipeline lines due to their unprofitability. This can probably be explained by falling gas prices due to favorable weather conditions.

Returning to the role of American LNG, it is worth paying special attention to Poland. At the end of January 2023, the Polish energy company Orlen signed an LNG supply agreement with the American raw materials corporation Sempra. This agreement is a long-term one, since the provisions of this contract come into force as early as 2027. According to these provisions, 1 million tons of LNG will be supplied to Poland annually. In addition, as of January 2023, the United States already turned out to be the main exporter of LNG to Poland, since the concluded contracts with Chenier and Venture Global already imply annual exports of at least 3 million tons.

Among other things, Orlen is slowly but surely pursuing its set course towards creating its own gas fleet: in 2023 the company should receive two tankers, and two years later their number should reach eight vessels for transporting LNG. What is noteworthy is that the interests of foreign capital demonstrate their transnational nature here too, because in addition to the American supplier itself, this agreement involves South Korean capital (Hyundai Heavy Industries was engaged in shipbuilding) and, again, Norwegian capital (transportation is carried out under a charter agreement with Knutsen OAS Shipping).

Turning to the technical characteristics, it is worth noting that each ship will transport 70 thousand tons of LNG: hypothetically, this is what all Polish households consume per week. By the end of January 2023, Poland received LNG from the terminal in Świnoujście, but its capacity is limited by regasification at a rate of 5 billion m³ per year (by the end of the year its capacity is planned to increase to 8.3 billion m³). But it is worth remembering that with the capitalist method of production, excess profits are at the forefront, and during certain periods, as was the case in the first half of 2022, owners of means of production and subsoil can completely reduce oil and gas production, taking advantage of increased exchange prices.

Of course, this process is not discreet and linear: the refusal of Russian gas, no matter how paradoxical it may sound, was associated with an increase in its purchases. The UK and a number of EU countries, including Germany, according to the German financial and economic daily Handelsblatt, purchased 21% more Russian gas in 2022 than a year earlier.

However, this did not at all prevent it from concluding a contract with Qatar at the end of 2022 for LNG supplies for a period of 15 years.

II. Alternative sources of gas

In addition to this contract, there is another obligation between Germany and Qatar, which concerns the supply of LNG from 2024 from the Golden Pass facility in Texas. The reader may be wondering: what is the connection between the state of Texas and a country in the Middle East? Especially in the context of hostilities in Ukraine.

The answer to this question lies in the economic plane: most of the shares in this installation belong to the Qatari state-owned company Qatar Energy. In the strict sense of the word, this is still the same American gas, which, as follows from the above, is currently systematically replacing Russian gas.

Moreover, the example of this state-owned company is of research interest as it enters into agreements with other capitalist sharks. A striking example from recent history is the signed contract between the French TotalEnergies, the Italian Eni, and the Lebanese government for the development of oil and gas fields in the economic zone of Lebanon, signed on January 30, 2023. LNG is also produced in Algeria. In fact, we are talking about a cartel conspiracy.

In addition to Middle Eastern Qatar, a gas alternative for Europe is Africa, or more precisely the state of Mozambique, where in 2010–2012 the largest natural gas deposits on the continent were discovered, after which their active development began.

At the same time, such companies as the Italian Eni, the American Anadarko and ExxonMobil, the French Total, the Portuguese Galp Energia, the South Korean Kogas, and the Chinese CNPC participate as miners and processors. The British transnational giant British Petroleum acts as a practically monopoly buyer (more precisely, reseller) of gas.

At the beginning of 2021, the development of Mozambican gas was temporarily interrupted by unknown local islamists that took control of the city of Palma in the Cabo Delgada region, where the French Total operated. However, they were reportedly soon suppressed by local government forces with the assistance of the British security firm Control Risk, and the French company continued construction of the gas processing plant.

In November 2022, the first tanker with LNG already left for Europe, and the President of Mozambique announced that “Mozambique is included in the annals of world history as an LNG exporting country.”

At the beginning of 2023, the head of the Italian energy company Eni, Claudio Descalzi, recommended that the European Union “pay attention not to the United States, but to Africa” to replace Russian energy resources and indicated that close cooperation with it “will create an energy axis... that will connect the resource-rich continent with energy-intensive European markets."

Well, we can add that this “close cooperation” will certainly and first of all allow capital to acquire always-in-demand markets for resources, cheap labor, and sales.

Another, no less textbook example associated with one of the leading American raw materials companies, Chevron, forces us to come to the same conclusions. The US authorities removed the Dragon gas fields in Venezuela from sanctions, and the Chevron corporation received a license to produce oil and gas in Venezuela at the end of January 2023. As the Reuters news agency notes, this means the possibility of renewing business agreements with Venezuelan state-owned companies for gas - and oil production.

Such companies, as can be seen from the same January news reports, are the Venezuelan company PdVSA, which, together with Chevron, is supplying gas to the American domestic market, while the mining industry of the United States itself is becoming, in turn, more and more export-oriented. To a certain extent, a similar situation is observed in South America, where Trinidad and Tobago ranks sixth among the largest LNG producers, 65% of which is supplied there, to the United States.

But if the example of Mozambique and Trinidad and Tobago hardly looks surprising, given the historically established relations between former colonies and metropolises, then deals with post-Chavista Venezuela testify to the goal of reselling (and to their own citizens) vital natural resources as expensively as possible, regardless of reputational losses. After all, when the opportunity to make a big profit is at stake, then a business conversation from the series “nothing personal - just business” can be started even with a “geopolitical enemy”.

To be fair, Michael Wirth, who serves as CEO of Chevron, on February 28, 2023, reported on the possible political risks associated with increasing mining operations in Venezuela. But what can “certain risks” mean when the prospects for increasing oil production from 250 thousand to 400 thousand barrels are at stake?

An even more egregious incident involving the “powers that be” is the accusation against Shell (and at the same time the Vitol trader) of “delaying Russia’s ‘Special Military Operation’ [approx. PSh] in Ukraine.” The accusation, oddly enough, came from the Ukrainian side: indignation was voiced by the economic adviser to the President of Ukraine, Oleg Ustenko. The charges put forward state that this oil company resold petroleum products purchased from Turkish refineries, which, in turn, are actively working with Russian oil.

Still, such statements from the current Ukrainian authorities should hardly be taken seriously. Almost a year earlier, Ustenko threatened such major Western banks as Goldman Sachs and JPMorgan with legal proceedings for purchasing Russian government bonds and even “preventing” them from carrying out financial transactions in Ukraine.

However, after just a couple of months, in the fall of 2022, both banks held meetings personally with the current President of Ukraine, Vladimir Zelensky, at a completely official level. Thus, they actually became one of the investors who will be able to invest enormous amounts of money in the Ukrainian economy. To put it more precisely, to finally bring it to a state of total credit enslavement.

In this regard, the aspirations of the same Ukrainian side to “share profits”, voiced in the spring of 2023, look especially ridiculous.

III. Interweaving of capitals

If, based on the above, one might get the impression that “Western capital” is something delimited and purely hostile to Russian capital, then this is not so. The imperialist stage, in which world capitalism currently finds itself, is precisely distinguished by the worldwide, transnational interaction of the capitals of different countries, despite even the formally hostile policies of these countries towards each other. The energy industry is no exception. We will cite only a number of facts known from publicly available sources.

Thus, as of spring 2023, British Petroleum still holds shares in Rosneft and receives dividends on shares, while taking virtually no participation in the activities of the Russian state-owned company.

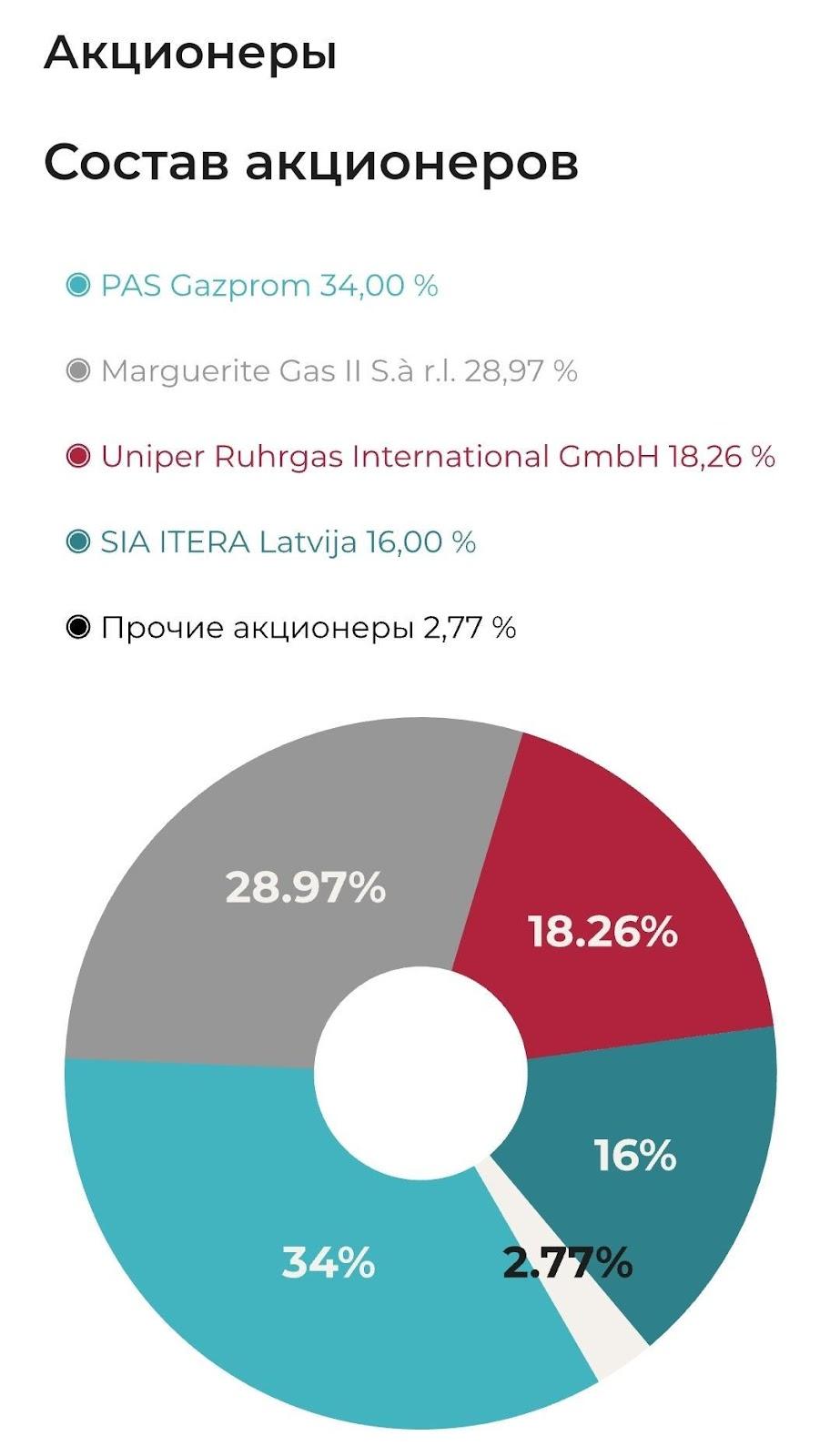

Russian raw materials companies, in turn, still maintain a virtual monopoly position in the Baltic energy sector. So, for example, in the shareholder structure of Latvijas Gāze, Gazprom continues to hold a share of 34%, remaining the beneficiary of this company.

Typically, the NASDAQ exchange in March 2023 reported the net annual profit of the Latvijas Gāze concern in the amount of 39.037 million euros ($43.096 million). According to the exchange, compared to 2021, net profit increased 12 times. Thus, the concern demonstrated record profits - and this against the backdrop of an equally record increase in prices for heating and electricity.

Looking at the diagram above, it is not at all difficult to guess who became the main recipient of dividends. This was at the very time when a massive campaign to demolish monuments to Soviet soldiers took place in the three once-Soviet Baltic republics. What can we say about the refinery owned by Lukoil in Bulgaria, the processed raw materials from which eventually ended up in the gas tanks of armored vehicles of the Armed Forces of Ukraine?

The same piece of the pie that Western and Russian capitalists are still able to “peacefully” divide among themselves is the fields in the Caspian region, as evidenced by the payment of dividends to shareholders for the past 2022.

IV. Western capital is driving Russia out of Europe

However, these, albeit bizarre, but still private phenomena do not cover the overall picture: the fact of the redistribution of the European oil and gas market. The turning point for this process was the events of February 2022. At the same time, it is not certain if Western capital won’t try to get the above-mentioned sales markets in the Caspian Sea and the Baltic States.

And most importantly, very soon the hour will strike for Western energy companies in Ukraine itself. Last summer, negotiations were held between the head of Naftogaz, Alexey Chernyshov, and the American companies ExxonMobil, Halliburton, and Chevron to increase gas production in Ukraine. According to Ukrainian officials, these measures would allow gas production by Western companies to quickly replace Russian supplies to Europe.

Less than a year had passed since Chernyshov held a second round of negotiations in Washington with representatives of the above-mentioned companies. As follows from an interview with the Financial Times, the subject of negotiations was the entry of American commodity companies into the Ukrainian market with the subsequent expansion of investment activities. According to Chernyshov, “We are working on an insurance mechanism to protect their capital.”

Thus, it can be stated that military actions in Ukraine are not an obstacle to the expansion and deepening of capital cooperation between formally hostile countries on the basis of resource development, despite their location in the field of these military actions.

V.I. Lenin, a hundred years ago, in his work “Imperialism, as the Highest Stage of Capitalism”, in the chapter “Export of Capital”, described the true goal and purpose of investments of large monopolies in other countries:

“As long as capitalism remains what it is, surplus capital will be utilised not for the purpose of raising the standard of living of the masses in a given country, for this would mean a decline in profits for the capitalists, but for the purpose of increasing profits by exporting capital abroad to the backward countries. In these backward countries profits are usually high, for capital is scarce, the price of land is relatively low, wages are low, raw materials are cheap.”

If we recall our recent article about the interests of Russian capital in Ukraine, about the relationship between Western and Russian capital there, it becomes quite obvious that the issue of dominance over the Black Sea shelf and coal in the Donbas has turned Ukraine into a bone of contention.

These and many other circumstances and events on the economic front for 2022 - the first half of 2023 indicate that Russia's ‘Special Military Operation’ and the subsequent sanctions against Russia freed the hands of Western capital and gave an incentive to increase oil and gas production in dependent and semi-dependent countries.

In light of the stated facts, the main question remains to be answered: who ultimately benefited the most from the redistribution of European commodity markets?

This is the American raw materials corporation ExxonMobil. As stated in the annual report, the company earned $56 billion in 2022, exceeding the 2021 figure by 2.4 times. Thus, a fragment of the former Rockefeller oil empire (Standard Oil), which continues to exert a colossal influence on US foreign policy, is still a confident leader on the list of the world's leading mining corporations.

The second place is occupied by the British raw materials monopolist Shell. The net profit of this giant exceeded last year's figure by 2 times, increasing from $20 to $42 billion. Revenue increased by 45.8% to $381.31 billion against $261.5 billion a year earlier.

The third place was taken by the French corporation TotalEnergies. Its net annual profit amounted to $36.2 billion, exceeding that of 2021. Revenue growth from fuel sales was 43%. On the oil and gas Olympus, it is adjacent to the American Chevron, which reported $35.5 billion in profit at $18.28 in diluted share value, thereby also significantly exceeding the net profit for 2021: $15 billion and $8.14 in share price, respectively. Chevron is the same raw materials TNC to which the US ruling circles granted a patent for oil and gas production in Venezuela. At the same time, according to the text of the annual report, the company also set record volumes in oil and gas production in the United States itself.

British Petroleum closes the list of record holders: the oil and gas, petrochemical and also coal transnational monopoly of Great Britain, which managed to amass a profit of $28 billion in 2022, reaching the record levels of 2008.

It is worth noting separately that this figure is a record for this oil and gas company over the past 115 years. In this regard, it is worth clarifying that this company has not yet left Russia: it retains a 20% stake in Rosneft. On the question of patriotism and the “total struggle” against the West for the survival of Russia: could Hermann Goering, at the very height of the Battle of Kursk, have been a shareholder of the Baku fields in the Soviet Transcaucasus?

In total, the annual net profit of these five is about $200 billion. The reason for such stunning excess profits lies in the rapid rise in energy prices. The occupation of commanding heights by Western oil and gas TNCs in the European (and not only) commodity market is the best possible confirmation of the correctness of comrade Stalin, when he revealed the basic economic law of capitalism in its highest stage – imperialism:

“The main features and requirements of the basic economic law of modern capitalism might be formulated roughly, in this way: the securing of the maximum capitalist profit through the exploitation, ruin, and impoverishment of the majority of the population of the given country, through the enslavement and systematic robbery of the peoples of other countries, especially backward countries, and, lastly, through wars and militarization of the national economy, which are utilized for the obtaining of the highest profits.

It is said that the average profit might nevertheless be regarded as quite sufficient for capitalist development under modern conditions. That is not true. The average profit is the lowest point of profitableness, below which capitalist production becomes impossible. But it would be absurd to think that, in seizing colonies, subjugating peoples, and engineering wars, the magnates of modern monopoly capitalism are striving to secure only the average profit. No, it is not the average profit, nor yet super-profit – which, as a rule, represents only a slight addition to the average profit – but precisely the maximum profit that is the motor of monopoly capitalism.” — I.V. Stalin, “Economic problems of socialism in the USSR,” 1952.

Words by I.V. Stalin, as we see, remains relevant today. Capitalist policy, as before, is inevitably associated with increasing militarization and the emergence of military conflicts, the export of capital to other countries, and the development of new markets, and the constant growth against this background of the profits of the big businesses involved. In parallel, with a decline in the standard of living of ordinary workers under the yoke of inflation, debt, tax levies, and all the problems associated with the involvement of the masses in the conditions of hostilities.

At the same time, the class nature of large transnational corporations is revealed by the fact that the ordinary EU citizen provides fabulous monopoly profits to corporations. After all, it is the proletariat of the European Union that ultimately pays the huge bills for gas and electricity, the money for which is then sent into the pockets of the resource monopolies. And don’t such EU republics as Germany or France lose at least part of their sovereignty and subjectivity, “getting rid of Russian energy dependence” and becoming completely energy dependent on “their” energy TNCs?

This does not even take into account the fact that in addition to the aforementioned all-powerful raw materials pentarchy, smaller predators, which were discussed above, also managed to approach the European gas market. For example, Italian Eni ($13.8 billion versus $8.4 billion a year earlier). We also mentioned Norway's new role as an exporter: the northernmost country on the Scandinavian Peninsula's hydrocarbon export revenues amounted to $147 billion in 2022, significantly beating last year's figures.

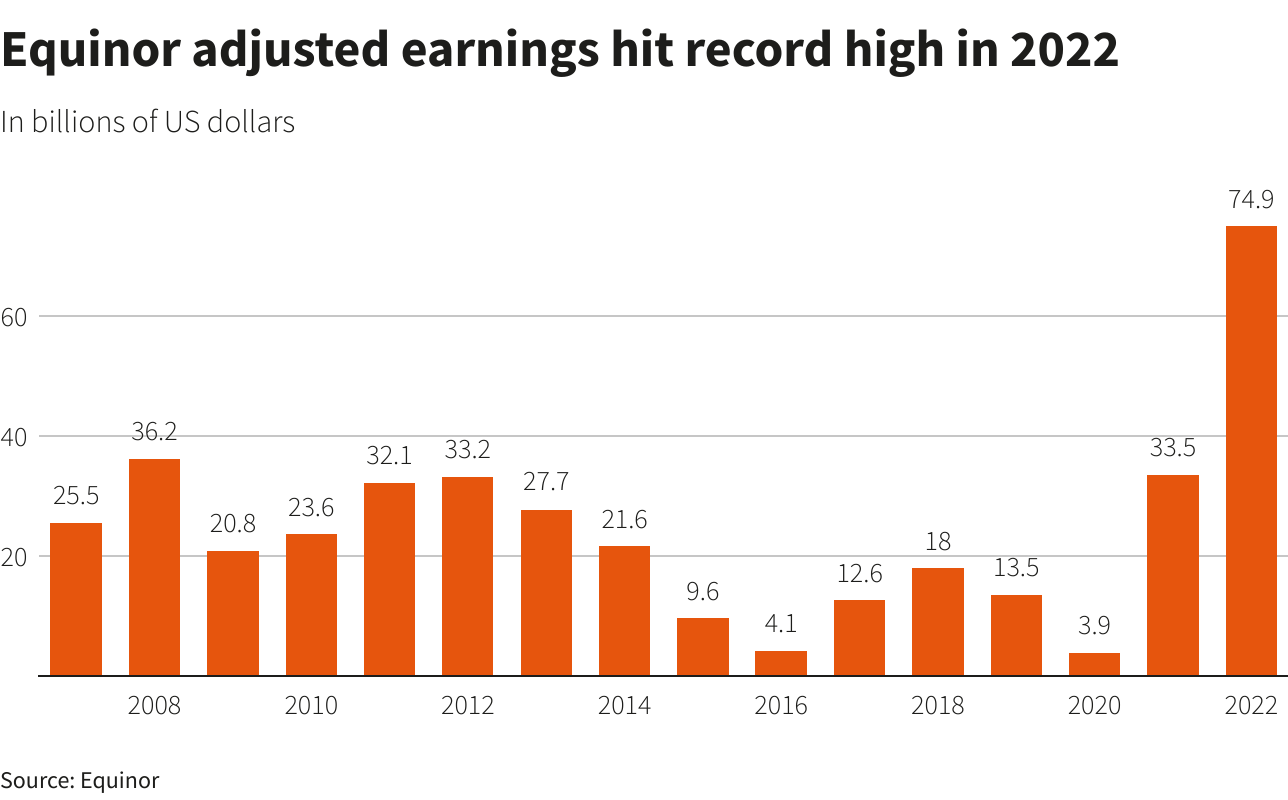

The beneficiary in the case of Norway is mainly the raw materials company Equinor, in which the state's share reaches 60%. According to the Reuters news agency, the Norwegian group's net profit for 2022 amounted to $28.7 billion compared to $8.6 billion a year earlier. In terms of adjusted operating income, the observed ratio was nearly $75 billion, doubling the 2021 figure.

What is characteristic is that in all these cases, analysts do not even hide the main source of such stunning and colossal profits: Russia’s withdrawal from the European commodity market and rising gas prices.

It becomes obvious that Western imperialism, largely for the sake of these intoxicating profits, agreed to the current conflict in Ukraine: this is the true price of talk about “energy independence of Europe” and “stopping sponsoring Russian aggression.” As you know, “there is no such crime...” when it comes to 300% profit.

In this regard, one important fact attracts attention. In all of the mentioned energy TNCs, without exception, the list of largest shareholders is crowned by the US financial elite. We are talking about the kings of Wall Street: the largest banks (JPMorgan, Goldman Sachs, Morgan Stanley, etc.) and investment funds, the most powerful representatives of which are the “Big Three” - BlackRock, State Street Corporation, and Vanguard.

Considering both their colossal influence on the political elites in Western countries and the rights of actual majority shareholders in the largest commodity TNCs, the conclusion about their purposefully pursued economic policy to redistribute commodity markets seems quite reasonable. A number of the above facts and circumstances make us think about a deliberately organized military conflict on the territory of Ukraine, in which the Russian Federation was presented as “extreme” in the eyes of the world community, hypocritically blaming it for the outbreak of hostilities.

The benefits of Western financial elites in this field are not at all limited to the profits of raw materials and even weapons companies.

The measures taken during the Ukrainian crisis have a long-term basis: the threat of a new jump in electricity prices will push declining industries to move to the United States, where they are kindly prepared for a more loyal and preferential financial policy. This is fraught with the notorious “brain drain,” and with it, productive capacity. This process can rightfully be called a new milestone in the era of imperialism, when capital is exported not only to backward countries but also to the metropolis.

In this regard, in the interests of big business tycoons, a series of neoliberal reforms will continue in the EU countries, including pension reforms, a striking example of which is the pension reform in France in 2023. The aforementioned almighty BlackRock already manages the EU pension program, the management functions of which were carefully entrusted by the European Commission to this largest investment fund in the world. This will make it possible to “free up”, or rather, return to the labor market crowds of pensioners who will be forced to struggle for existence in search of funds to pay for utilities.

This indicates that measures are being prepared to introduce a regime of “austerity” primarily in the EU countries: the state’s share will be systematically reduced, claiming only the role of a night watchman. The public sector will, at best, absorb purely “unprofitable” enterprises. Nationalization of losses, privatization of income.

In this sense, events in the economy of post-Maidan Ukraine may be a prototype of the upcoming transformations in the EU. It is possible that the facts of nationalization of the assets of Kolomoisky, Boguslaev, and some other Ukrainian oligarchs may prepare the ground before the arrival of much larger predators from overseas.

In conclusion

What conclusions can be drawn from the above?

- The final transition from the “Russian raw materials needle” to the Western one is a matter of time, and the construction of the required number of LNG terminals and pipeline routes is a matter of technology;

- The main gas suppliers to Europe in 2022 - the first half of 2023 were the USA and Norway;

- If this is beneficial to the owners of Western raw materials TNCs, then “Europe will not freeze,” despite the exhortations and howls of Russian government propagandists. The issue of affordability is not a priority for the biggest tycoons in the global electricity market, which can also be explained by their monopoly position;

- In search of alternatives to Russian gas, Western transnational resource corporations have intensified the exploitation of production capacities in countries such as Venezuela, Mozambique, Lebanon, Algeria, Trinidad and Tobago, etc., and at the same time, the exploitation of workers there;

- The world community turns a blind eye (or does not even know about them) to the crimes of pro-Western armed groups involved in local military conflicts in which the interests of mining corporations are traced;

- “Energy independence” has already cost the EU countries $1 trillion, which also affected the payment receipts of EU citizens. Increasing prices for electricity and gas are signs of the general impoverishment of the proletariat, both in relative and absolute forms;

- The abandonment of Russian oil and gas is not a linear process at all, which can be explained, for example, by bidding on the price of different grades of Russian oil on different exchanges. In addition, the Russian big bourgeoisie, represented by the Kremlin oligarchy and the top management of state-owned companies, are looking for any loopholes to continue the export and transit line to the EU countries, including through India, Belarus, and even Ukraine;

- The total annual net profit of the five largest commodity TNCs - ExxonMobil, Shell, British Petroleum, TotalEnergies, and Chevron in 2022 exceeded $200 billion. Such profits became possible due to the conquest of a monopoly position in the European market and rising energy prices;

- These companies are already making plans to enter the Ukrainian market after the end of Russia’s ‘Special Military Operation’;

- The beneficiaries of these companies, in turn, are building long-term plans for the further reconstruction of Europe, which go far beyond the commodity sector.

All these fundamental changes in the global balance of power of the imperialist powers are accompanied by bloody conflicts and a sharp decline in the material well-being of the working people. An alternative to such an outcome, when billionaires make money on the suffering of millions of people, can only be a socialist system. Only with the victory of socialism throughout the world and the establishment of a world Soviet republic will it be possible to put an end to the bloody “games” of the rich.

Sources:

- Gas-Batyushka: Taking leaps and bounds towards independence from gas from the Russian Federation — from January 21, 2023

- Gas-Batyushka: Germany continues to build new LNG terminals - environmentalists are against - from March 20, 2023

- Gas-Batyushka: “News in Brief” - from November 16, 2022

- Gas-Batyushka: “News in Brief” - from February 6, 2023

- RBC: “Electricity bills in Europe have reached record levels” - from November 7, 2022

- Vedomosti.ru: “Bloomberg: Europe’s losses from rising energy prices amounted to $1 trillion” - from December 18, 2022

- Banksta: “In Germany, the share of Russian gas fell to 20% over the year” - from December 20, 2022

- Banksta: “The share of Russian gas in the Czech Republic has decreased over the past year from 97% to 4%” - from February 1, 2023

- Deutsche Welle: “The Baltic Pipe gas pipeline was opened in Poland” - from September 27, 2022

- Deutsche Welle: “Now it’s clear how Norway helped Germany replace gas from the Russian Federation” - from January 24, 2023

- Warsaw Mermaid: “Energy bondage of the Poles” - from January 26, 2023

- Warsaw Mermaid: “Poland imported record amounts of liquefied natural gas last year” - from January 9, 2023.

- Handelsblatt: “The EU and Britain have increased LNG imports from Russia by 21% since the beginning of the year” - from December 6, 2022.

- Reuters: «Chevron sending two oil tankers to Venezuela under U.S. approval» — from December 20, 2022

- Gazeta.ru: «Reuters: Тринидад и Тобаго увеличил экспорт СПГ в Европу в два раза в 2022 году» — from June 29, 2022

- Reuters: «Chevron’s output gains in Venezuela limited by political risk, CEO says» — from February 28, 2023

- Novyny Live: Shell and Vitol were accused of prolonging the war with Ukraine: what is the reason — от February 19, 2023

- Epravda:: Ukraine will bring war crimes charges against Western bank executives over Russian financing — from June 27, 2022

- Official Internet representation of the President of Ukraine: Vladimir Zelensky met with representatives of the investment company Goldman Sachs — from October 20, 2022

- Official Internet representation of the President of Ukraine: Vladimir Zelensky met with top managers of JP Morgan and took part in an investment summit organized by the holding company — from February 11, 2023

- Gas-Batyushka: Ukraine wants to receive part of the profits from global energy giants — from March 30, 2023

- Tvnet.lv: The profit of Latvijas gāze increased 12 times last year — from March 3, 2023

- Rybar: Romania becomes the largest fuel supplier to Ukraine — from February 15, 2023

- Caspian Pipeline Consortium: On payment of dividends to CPC shareholders — from December 8, 2022

- Gas-Batyushka: Have American companies started dividing Ukrainian energy resources? — from April 23, 2023

- ExxonMobil News: «ExxonMobil announces full-year 2022 results» — from January 31, 2023

- Reuters: «Shell 2022 profit more than doubles to record $40 bln» — from February 2, 2023

- Offshore Technology: «TotalEnergies annual profit doubles to $36.2 bn» — from February 2, 2023

- Chevron Newsroom: «Chevron announces fourth quarter results» — from February 9, 2023

- Reuters: «BP makes record profit in 2022, slows shift from oil» — from February 7, 2023

- Eni, Board of Directors Communications: «Eni: fourth quarter and full year 2022 results» — from February 23, 2023

Reuters: «Equinor shares spike as gas bonanza lands record profit» — from February 8, 2023